Эта статья опубликована под лицензией Creative Commons и не автором статьи. Поэтому если вы найдете какие-либо неточности, вы можете исправить их, обновив статью.

Contribution of Inventory Accounting Systems in Improving Inventory Internal Control

Ade Onny Siagian

Опубликована Янв. 1, 2020

Последнее обновление статьи Ноя. 17, 2022

Эта статья опубликована под лицензией

")

Abstract

The purpose of this study was to determine the Role of Inventory Accounting Systems in Improving the Inventory Internal Control Structure at Putri Mayasari Cilandak. The research method used in this study is a qualitative research method with a case study approach and the data collected consists of primary and secondary data. Then Primary Data is collected through interviews, observations, and documentation, while Secondary Data is collected through library research to determine the role of the inventory accounting system in improving the structure of internal inventory control. The results of the study found that the role of the inventory accounting system in improving the internal control structure of inventory has been implemented properly and correctly.

Ключевые слова

Inventory, Internal Control, Accounting System

NTRODUCTION

In the rapid development of technology, Trend of increasing community needs and world development that leads to globalization, so will affect to Indonesian economy and the level of bussiness competition, based on economy development, so sophisticated technology very be needed in economy field who be felt that development very rapidly. While Indonesia's condition lately face serious problems for the future of nation life. The prolonged economic life crisis will directly affect the progress of a company. So this must be recognized as an economic problem that is going well according to the condition of this nation.

The growth and development of industrialization is amazing. Industrialization has given opportunities to the community to get a better life extensively with adequate income.

Meanwhile the government receives revenue from tax as capital to accelerate the national development process. Then developments in Indonesia are also influenced by international developments, where Indonesia as one of the countries in the world experiencing the effects of globalization due to economic activities at the international level. In the Indonesian economy, companies are one of the strengths and actors of economic must increase product productivity and quality in so that can face the global competition that will be faced. So in this connection what is meant by companies are manufacturing companies and trading companies. Where manufacturing companies are companies whose activities convert raw materials into finished products/finished materials, while a trading company is a company whose activities are in the field of buying and selling goods. Then besides increasing productivity and product quality the company must also improve handling of internal or market understanding, part of market and partners in running their business.

While handling of internal is handling which includes what, how much, where and how. The product also results in the handling of an accounting system as an information system for determining company policy. Putri Mayasari is a Home Industry company whose business activities are engaged in the snack food industry, then in an economic situation like this has an important role in supporting the growth of the company, especially in the industrial sector which can increase the growth speed of regional economic. It is known that Putri Mayasari has a fairly large place, so the economic structure will become very complicated and its complexity will continue to increase along with development and many activities carried out, so the scope of company's operations will be more extensive and complicated, then to evaluate operations effectively management requires a variety of reports and analysis. Therefore, we need a tool that can produce information that is timely, relevantly and orderly, so can help manager in run company's activities. The accounting system is the process of identifying, measuring and reporting economic information to enable clear and firm judgments and decisions for them who use that information. (SR, 2005).

Based on that statement, implementation of an inventory accounting system and internal control structures are very important in providing information and avoid buildup and inventory and avoid production or transaction decline. Knowledge of accountancy is very important and be needed to manage business operational. (Siagian & Indra, 2019).

Internal control is one of the tools who be used to evaluate the management effectiveness of a company. Internal controls are policies and procedures that protect company's assets from misuse, ensuring that business information that be presented is accurate and convincing that have followed laws and regulations, that's According to Carl S. Warren, James M. Reeve, Philip E. Fess in (Warren & Fess, n d ). While according to (Arens, Alvin., Randal J.Elder, 2008), The internal control system consists of policies and procedures designed to provide appropriate management certainty taht commpany has reach goals and target. Through this internal control, part of company management can know the extent to which implementation of company effectiveness has been achieved, problems in the company and manner to resolve that problem. Internal control is the whole plan of the organizational structure and all methods related to coordinated within a company that supports to obtain company assets, and also the method of accuracy of leadership policies that have been determined (Mulyadi, 2010). According to (Mulyadi, 2010) that There are four main elements of the internal control system that is:

- An organizational structure that separates functional responsibilities explicitly.

- A system of authority and recording procedure that provides adequate protection against wealth, debt, income and costs.

- Healthy practices in carrying out the duties and functions of each organizational unit

- Employees whose quality is in accordance with their responsibilities.

Therefore, be needed effective and efficient mangement in distribution of goods and services and need handling by the wise and honest people with authority and responsibility clearly as well as the separation of functions in order to minimize the occurrence of fraud and irregularities committed by unhealthy practices such as waste, embezzlement, theft and things that can cause harm to the company it self.

METHOD

The research method used by researchers is to use descriptive analysis research with the case study approach

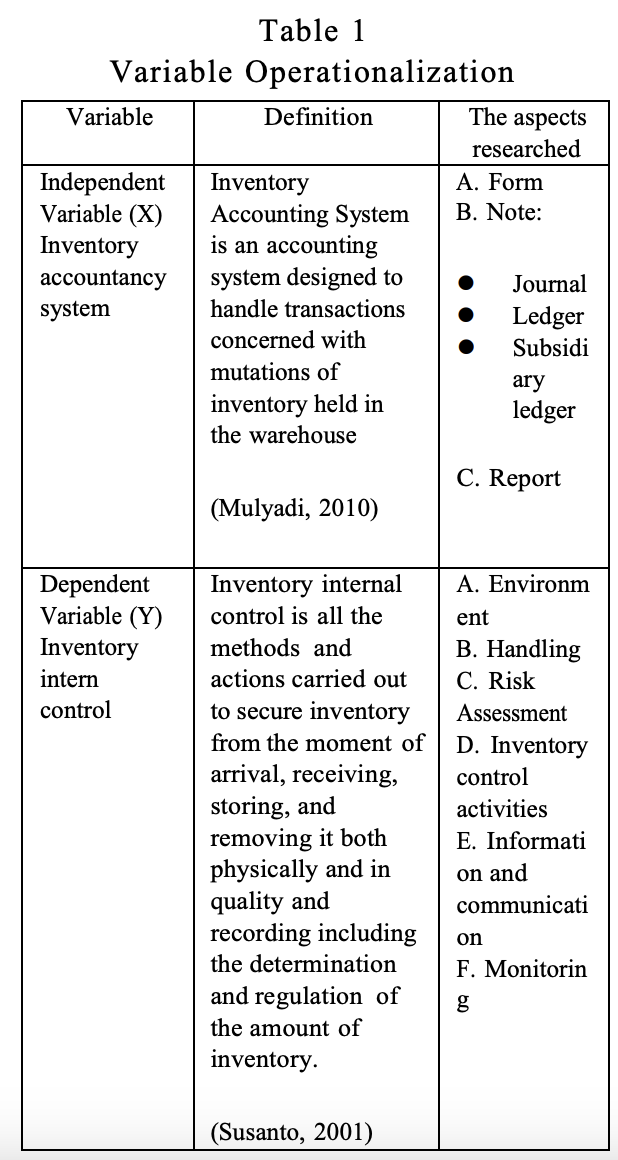

This study uses two variables, where the independent variable X is the Inventory Accounting System, and independent variable Y is inventory internal control structure.

For more information, see the operational variables table below:

RESULTS AND DISCUSSION

This accounting system is the embodiment, compilation, collection and summarization of information which links all transactions and involves employees, activities, forms, reports and procedures that have been determined so that they can obtain effective information. In addition, the accounting system can be said to be effective if it meets the elements of the accounting system, that is: forms, notes, and reports

- Form

Based on research, the form used by Putri Mayasari is made simple, concise and clear, making it easier to fill and record every transaction that occurs. In Putri Mayasari in this form, noted among other things: various raw materials, the large number of raw materials per kilo to be purchased in accordance with the order, and stock of raw materials that have been issued, as well as other information that supports the management of inventory. From these explanations in general the forms and documents used in the accounting system have been quite effective.

- Notes

The notes used by Putri Mayasari are the journals used in supporting the inventory of goods in Putri Mayasari are as follows:

a) Journal

The recording is made from the recording in the basic document, namely the form, which is then directly recorded in the accounting program where the recording is recorded through software that functions the same as a journal, namely the first recording of the transaction. Besides posting on the software.

b) Ledger

It is a computer engineering which is posted and made at the end of every month and the result is a print out containing accounts that are used to summarize data that has been previously flawed in the ledger, and is a source of financial information for the presentation of financial statements.

c) Subsidiary Ledger

Subsidiary ledger has been used in computer engineering, which function remains as supporting information in the general ledger. Therefore this computer engineering is a control accounts detailing financial data for the presentation of financial statements.

- Report

All activity on goods inventory who have been done by Putri Maysari Cilandak is noted and summarized to into report form which is the main task of the Head of Data Warehouse and Administration. Reports be made by Putri Mayasari regarding inventory management activities include: Goods Receipt Details Statement, Item Expenditures Details Statement, Income Statement (L/R).

From the results of this research it can be concluded that the inventory accounting system at Putri Mayasari Cilandak is quite effective. This can be seen from the existence of forms, notes in the form of journals, ledgers and the existence of inventory reports and supported by computer electronic equipment as a tool in processing data that is in the company

Putri Mayasari in ar anging that intern control structure has tried to give attention to the elements of the internal control structure itself. This can be seen from the control elements below, that is:

- Control Environment

The control environment that occurs can create an atmosphere of control within the organization of Putri Mayasari and affect the organization's personal awareness about controlling the supply of raw materials. The various factors that make up the inventory control environment at Putri Mayasari are as follows:

a) Integrity and Ethics

There are rules that are applied by Putri Mayasari both in writing and otherwise that must be obeyed and implemented by all employees in this company when the operational takes place. In order to create discipline and honesty for its employees. So that create discipline and honesty for its employees.

b) Management philosophy and operating style

Management philosophy and operating style who be done by this company have given direction and confidence for each student in running activity of operational with their respective assignments. Beside that, the management philosophy desired by management is the policy of the company's to bring its employees towards what this company wants. Whereas the management operating style used is to instill the importance of financial reporting that makes its employees have professional responsibilities.

c) Organization Structure

Putri Mayasari's organizational structure shows that the planning of the controlling and monitoring of activities is in the hands of the company leadership below which there are parts of the task that have been arranged to assist the implementation of the company's activities.

d) Delegation of Authority and Responsibility

The delegation of authority and responsibility of Putri Mayasari has been implemented well, where each part of the assigned task has the authority and responsibility in accordance with the work environment.

- Risk Assessment

Putri Mayasari has always been meticulous in making decisions, policies and actions regarding inventory activities. The accounting data produced by the company regarding inventories is sufficiently reliable by Putri Mayasari's management in conducting an analysis to calculate the risks that will be faced if management determines the decision. This is very important in the condition of the company, seeing the many obstacles and opportunities that exist in inventory activities when facing fraud/theft both of a raw material and production material and prevent management record errors.

- Control Activities

Putri Mayasari carries out an effective separation of the parts directly involved in the supply of raw materials in the form of a division of tasks that records the amount of

incoming and outgoing raw materials handled by the warehouse with the part recording the cost of goods with each type of inventory entering or exiting which is handled by the administration staff of inventory recording. In addition, every transaction that occurs in the company is always accompanied by documents and reports as one of the implementation of the system in force in the company and the existence of physical control over assets and records, as well as independent checking of inventory.

- Information and Communication

Putri Mayasari in accommodating the implementation of the information and communication system for inventories has determined the elements of the inventory, which include: Forms, records and reports on inventory management. So that the information and communication system that is in Putri Mayasari runs well and correctly in its implementation.

- Monitoring

Based on the results of Putri Mayasari's management monitoring of all activities in the company, namely by looking directly at and checking the similarity of records with inventory activities in the field and inventory activities in the warehouse or by checking existing data in the computer to get the same results based on cross-check data. In this case the results of physical calculations carried out by the inventory count team in the warehouse section determine internal control, so that it can continue to be monitored through cross checking of warehouse books and inventory books with the results of physical inventory calculations.

A. The Role of Inventory Accounting Systems in Increasing Inventory Internal Control

The accounting system is an element that forms the structure of internal control. Judging from the accounting system we can classify, analyze, and record and report transactions. Similarly, the inventory accounting system. From the inventory accounting system, we can find out that the amount and type of inventory the company has can find out the transactions that occur. The elements contained in the inventory accounting system can be used to check the superiority of accounting data that has been made and secure inventory. The elements contained in the inventory accounting system can be used to check the superiority of accounting data that has been made and secure inventory.

This is in accordance with one of the objectives of the internal control structure, namely checking the superiority of accounting data and securing assets. Based on the organizational structure and procedures that have existed at Putri Mayasari, in the holding of inventories is the authority and responsibility of the accounting and management accounting department in coordination with the terminal section responsible for the equipment section which includes control activities to be carried out efficiently and effectively so that cost savings can be achieved properly.

An effective accounting system is needed by Putri Mayasari Cilandak's management to determine the condition of inventory in the company so that it can be used as a basis for decision making of company management.

Some information needs are met with an effective inventory accounting system. As the authors have described above, that the implementation of the inventory accounting system applied by Putri Mayasari has basically been quite effective. This can be seen from the organizational structure and job descriptions in the management of goods, the existence of procedures, forms, records and reports.

Internal control is implemented by Putri Mayasari to create fair accounting data, suppress the implementation of policies set by the company and improve the company's operational efficiency. Internal control in its application needs to be assisted by an effective accounting system so that all company activities can be carried out according to plan, especially in the implementation of inventory management activities. Internal control carried out by Putri

Mayasari can be said to be effective because it has fulfilled the elements of the internal control structure itself, namely the control environment, the risk of management establishing , accounting information and communication systems, control and monitoring activities.

CONCLUSION

The results of research and discussion on the Role of Inventory Accounting Systems in Improving the Internal Control Structure of the Company in Putri Mayasari Cilandak, that is: Inventory accountancy system exist in Putri Mayasari Cilandak already effective. This is because there are forms, records, and reports on supplies and be assisted with computer electronic tools as tools in managing existing data at the company. Internal control on inventory is said effective because the elements of internal control, that is: environment, application of risk management, information and communication, control activities, and monitoring. Then already implementated by management of company to create condition where each employes do task seriously, do implementation of risk carefully and order of activity corresponding with who has applied, and monitoring by managers to achieve company goals. With the existence of an inventory accounting system conducted by Putri Mayasari Cilandak has an important role in improving the company's internal inventory control.

REFERENCES

- Arens, Alvin., Randal J.Elder, M. S. B. (2008). Auditing dan Jasa Assurance (Jilid I, E). Erlangga.

- Mulyadi. (2010). Sistem Akuntansi. Salemba Empat. Siagian, A. О , & Indra, N. (2019). Pengetahuan

- Akuntansi Pelaku Usaha Mikro Kecil dan Menengah (UMKM) Terhadap Laporan Keuangan. Syntax Literate; Jumal Ilnriah Indonesia, -/(12), 17-35.

- SR, S. (2005). Akuntansi Suatu Pengantar (Edisi Lima). Salemba Empat.

- Susanto, L. M. dan A. (2001). Sistem informasi Akuntansi (Edisi Rede). Linggajaya.

- Warren, R, & Fess, P. A. F. (n d ). Amanugrahani dan Taufik Hendrawan. 2005. Accounting Pengantar Akuntansi.