Эта статья опубликована под лицензией Creative Commons и не автором статьи. Поэтому если вы найдете какие-либо неточности, вы можете исправить их, обновив статью.

Overview of changes in the taxation of agricultural producers In Russia

Oksana V. Vaganova

Svyatoslav V. Yevdokimov

Natalia E. Solovjeva

Опубликована Янв. 1, 2020

Последнее обновление статьи Сен. 22, 2022

Эта статья опубликована под лицензией

")

Abstract

Agriculture is one of the most important priority sectors of the national economy, which provides the country's foodsecurity. But there are many problems in the activ-ities of agricultural producers, connected to the general taxation regime and the large tax burden.The purpose of this article is to study the current Unified Agricultural Tax (UAT), identify the positive and negative aspects of the application of these special tax re-gimes, as well as identify the main instruments of state support for agricultural pro-ducers.The problems that were solved during the writing these work were to substantiate the feasibility of Unified Agricultural Tax introduction for agricultural producers, adapt-ing it to the real conditions of agricultural business, analyzing the terms that must be met during Unified Agricultural Tax application, as well as studying the variation in the rates of a single tax to identify balance between the burden on payers and the amount of tax revenues to the budget.The research is based on general scientific methods of empirical research, analysis and synthesis, analogy, systematization, as well as methods of structural and logical analysis.The authors described the field of key changes in the system of the unified agricul-tural tax, based on amendments to the Tax Code, and emphasize the taxation of agri-cultural producers’ property. The authors described in details subsidies and conces-sional lending to the agricultural sector of the economy, studying government sup-port for agricultural producers

Conclusions. The methods of government regulation of agriculture in Russia are quite diverse and each of them has its own advantages and disadvantages. There is no universal method because of the uniqueness and individuality of agricultural produc-ers. They depend on the place of production, its primary and subsequent processing. Consequently, the changes introduced to the Tax Code of the Russian Federation in the field of taxation of agricultural producers can affect both positively and negative-ly. Undoubtedly, the effect of these innovations will still be there, and it can be traced in future indicators of tax revenues of the Russian Federationbudget.

Ключевые слова

Agribusiness, VAT, agricultural producers, agriculture, unified agricultural tax, tax burden

Introduction

Agriculture is one of the most important priority sectors of the national economy, which provides the country's food security. Due to the fact, that agriculture directly affects the economic security of the state, it needs to be paid a lot of attention. And this industry has a lot of problems. They are: a rather wide range of fuel prices and lubricants, low profitability of agricultural production, low innovative and digital technologies level, poor living conditions of the rural population, as well as dumping food supplies from abroad.

To neutralize the above negative facts, governmental support for agricultural producers and for newly created agricultural organizations is required. One of the difficult moments in the activities of agricultural organizations is the general taxation regime and the large tax burden. Although there is a preferential tax regime prescribed in the Tax Code of the Russian Federation. Switching to the unified agricultural tax (70%) special conditions must be met. Not all participants in the agricultural sector can fulfill the special conditions prescribed in the Tax Code. As an example, we can cite the statistics for the Belgorod region. There was 5053.6 million rubles of the federal support allocated, and only 80% (4028.9 million rubles) was realized. After analyzing this situation the Ministry of Agriculture in the beginning of 2020 changed the government support program, in order to consolidate such areas as: “unified subsidy”, “subsidy for increasing productivity in dairy cattle breeding” and “unrelated support”. These directions will be implemented through compensatory and incentive subsidies [Subsidizing the agro-industrial complex in 2020].

The problems in the field of agricultural taxation in Russian science have been dealt with by many scientists and statesmen. Nevertheless, this problem is relevant nowadays. Moreover, the development of agriculture in the conditions of sanctions and pandemic is associated with a number of problems, which limit the export of our products to other countries. Consequently, these factors slow down the growth rates in agricultural production.

The purpose of this article is to consider issues related to the taxation of agricultural producers, studying of the objective nature of taxation in agriculture and the influence of innovative factors of unified agricultural tax on the efficiency of agricultural producers’ identification. The monographic method was used in the article in order to study problems, illustrate the barriers in the activities of agricultural producers and identify the positive and negative aspects of introducing a unified agricultural tax.

Discussion

At the present stage of the Russian economy development agricultural producers have a unique opportunity in planning their tax obligations, so they can choose a taxation regime. It can be general or special preferential. In order to take advantage of this taxation system, it is needed to be an agricultural producer. The category of agricultural producers includes peasant farms and individual entrepreneurs, whose type of activity is production, processing, and sale of livestock products, crop production, and fisheries. At the same time, production or sale activity is not obligatory - all companies and other forms of entrepreneurial activity that provide services in the field of agriculture are classified as agricultural producers.

It is needed to check the limitations and conditions for the application of unified agricultural tax for a more detailed study and identification dependence of the tax level on the efficiency of activities. Taxpayers using this system are exempted from paying income tax (individual entrepreneurs from personal income tax), and also partially from property tax [Declaration of the Agricultural Tax for 2019]. Along with exemption from income tax, there is an obligation to pay a unified tax from the difference in income and expenses. The main limitation that exists in the application of the UAT is the limitation of income from non- agricultural activities. Thus, the percentage of revenue from sales of agricultural products in the total amount should be at least 70%.

Due to the amendments to the Federal Law of November 27, 2017 No. 335-FL "On Amendments to Parts One and Two of the Tax Code of the Russian Federation and Certain Legislative Acts of the Russian Federation" [Federal Law of November 27, 2017 No. 335- FZ], which entered into force on January 1, 2019 entrepreneurs using the unified agricultural tax have an obligation to pay VAT to the budget. Until 2019, VAT was not provided for persons using the unified agricultural tax. Due to the last changes, companies and individual entrepreneurs using the unified agricultural tax will have to draw up all the necessary documents as payers of value added tax. It should be noted that this kind of documents includes a book of purchases and sales, invoices for counterparties, and a VAT declaration [Tax Code of the Russian Federation 2020].

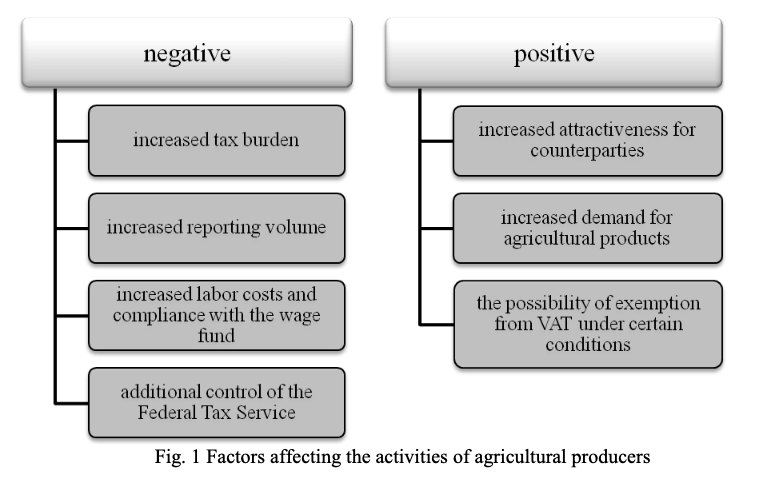

As agricultural producers need to pay VAT, it is necessary to realize how such an innovation will affect agricultural producers. Consider the negative and positive aspects of change in Figure 1.

Analyzing, first of all, the negative aspects of innovations, it should be noted that an increase in the tax burden and, consequently, reporting volume especially for small or microbusinesses in the field of agriculture could play a decisive role in reducing production or selling it to larger agricultural producers, which may subsequently negatively affect the competition market. In addition, it is worth noting that the unified agricultural tax is a unique taxation system, whose purpose is to develop national agriculture. But the additional control that will be exercised in relation to agricultural producers as persons paying VAT will strengthen control over agricultural businesses, and thereby will contradict the essence of the unified agricultural tax.

The expected positive effects of the VAT introduction for agricultural businesses should be mentioned separately. The market demand for products of domestic agricultural producers is a fairly stable value, therefore, the introduction of VAT will increase demand slightly or not affect the value of demand for agricultural products at all.

There are certain conditions under which persons paying the unified agricultural tax could be exempted from VAT, they include:

- notifications for getting an exemption from VAT and about the start of work using special regime should be related to one calendar year;

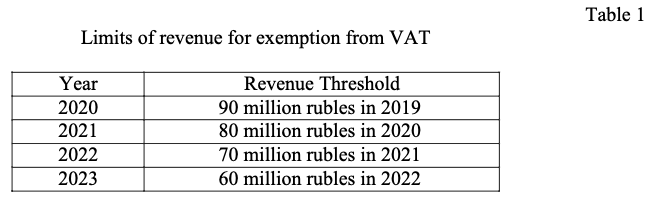

- compliance with the limit on revenue from agricultural activities. A gradual decrease of limits is planned [Declaration of the Agricultural Tax for 2019]. For example, to exempt from VAT in 2019, the threshold value of revenue for 2018 should have been not more than 100 million rubles, excluding taxes. The values of the revenue limits for obtaining exemption from VAT in the following periods are presented in Table 1.

- Filling notification of VAT exemption for the unified agricultural tax, which is submitted inclusively until the 20th day of the month from which the payer begins to use his/her right not to pay the tax. The application form for exemption from VAT with the unified agricultural tax in 2019 is given in the Letter of the Federal Tax Service of Russia dated 01.15.2019 No. SD-4-3/287@.

- Those agricultural producers who sold excisable products within three calendar months before the notification will not be entitled to VAT exemption.

It should be noted that if a person paying the unified agricultural tax sells any type of excisable goods or if it goes beyond the limits of revenue established by law, excluding taxes, then the right not to pay VAT is abolished. In the future, these companies and individual entrepreneurs will not be able to receive a second exemption from VAT. Moreover, the termination of exemption from VAT is possible only in cases of requirements and restrictions violation.

The unified agricultural tax in 2019 under general conditions was paid at a standard rate of 6%. At the same time, in the constituent entities of the Russian Federation from January 1, 2019, any value of the tax rate up to 6% can be established. The size of the tax rate depends on:

- the type of agricultural products (or works / services);

- the amount of income from doing business in the field of agriculture;

- places where an entrepreneur carries out activities;

- the number of employees of the company or individual entrepreneur.

Variation of rates allows agricultural producers to find a balance between the burden and the amount of tax revenue. Certain regions of the Russian Federation have already introduced reduced tax rates for the unified agricultural tax [Current problems of taxation of agricultural businesses, 2019]. For example, in the Moscow Region, a zero tax rate is established until December 31, 2021. Moreover, in the Kemerovo region the rate of the unified agricultural tax is 3%, and in the Belgorod region - 6%.

An important issue in applying the unified agricultural tax is property taxation. In recent years, an amendment to the Tax Code regarding the property tax has been made as a key change in the unified agricultural tax system. Property which is directly involved in agricultural activities could be exempted from taxation. This property includes assets that are involved in the production, processing, sale of agricultural products or in the provision of services.

Property used in agricultural activities can be divided into two groups. The first group includes property which is directly used for production. For example, sowing equipment, buildings in which animals are kept, etc. The second group includes auxiliary property: equipment garages, warehouses, etc. The right not to pay the property tax is applied to both groups.

Property assets and assets related to agricultural activities must be accounted separately. However, a situation may arise when the company simultaneously uses the property for agricultural production and for other activities. In this case, it becomes impossible to account these assets separately. In 2018, a letter of the Federal Tax Service dated July 10, 2018 No. BS-4-21/13205@ was published. The document gives the following explanation: in cases when agricultural businesses use the property for other entrepreneurial activities, but at the same time for its intended purpose, the property is not taxed. In addition, there is no need to pay the property tax if the assets are mothballed, consequently, temporarily not involved in the main business.

Other innovations include: the right to pay the unified agricultural tax is granted to those who have vineyards; sellers of wines of their own production, and other alcoholic beverages containing grapes, including grape must; regulated tax revenues to the budget at the place of production of the relevant product, or its processing; fishery and fishing companies may take into account expenses of participation in the auction for the purchase of a share in the total volume of quotas for catching (producing) aquatic biological resources [Main directions of the budget, tax and customs tariff policy for 2020].

The tax receipts to the corresponding budget at the place of production of fish products or their processing have been fixed. Fishing and fish production businesses can take into account the expenses incurred during the auction to buy out a part in the total volume of quotas for catching (extraction) of aquatic biological resources [Main directions of budget, tax and customs tariff policy for 2020].

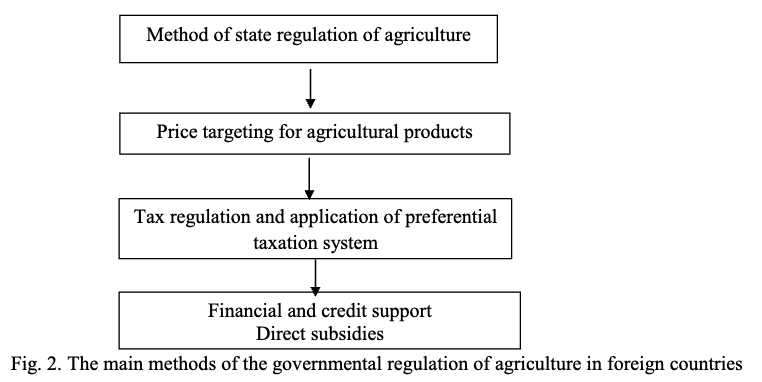

Studying the governmental support of agricultural producers in foreign countries, we should mention the developed subsidies to agriculture (Figure 2). But in the Russian Federation, there are quite a few methods of state regulation of agricultural producers. The methods are given in Figure 3.

The methods of state regulation of agribusiness in Russia are constantly under control of the Government. Undoubtedly, the Government of the Russian Federation establishes new rules of farming, which should help to intensify the activities of agricultural producers. Distribution of the unified subsidy developed by the Ministry of Agriculture in 2020 in order to in

crease its volume for some regions is one of these methods.

Nowadays, 72 constituent entities of the Russian Federation are subsidized and only 13 are not subsidized. The total amount of budget allocations has increased from 675,260 to 717,866 billion rubles. [http://fmcan.ru/articles/41_dotacii-regionam- rossii-2019/].

Not all regions have increased subsidies, for example, the Murmansk region has received smaller subsidies this year compared to the previous year (2019 - 32 million rubles, 2020 - 15 million rubles). The subsidies have increased in Dagestan (+6.626 billion), Sakha (Yakutia) (+4.691 billion) and Kamchatka Krai (+3.739 billion).

Another important method of stimulating agricultural producers is concessional lending, which is carried out by JSC Rosselkhozbank under the Program of State Support for Agricultural Businesses, approved by the Government of the Russian Federation dated April 26, 2019 No. 512.

Conclusion

The methods of state regulation of agribusiness in Russia are quite diverse and each of them has its own advantages and disadvantages. Of course, a universal method can’t be developed. Every agricultural production is unique and individual in its own way, depending on the place of production of agricultural products, its primary and subsequent processing. Consequently, the changes introduced to the Tax Code of the Russian Federation in the field of taxation of agricultural producers can affect positively and negatively the activities of agricultural producers. Undoubtedly, the effect of these innovations will still be there, and it can be traced in future indicators of tax revenues of the Russian Federation budget. «Russian agribusiness has several special tasks to accomplish, including digital transformation, pursuit of new niche markets and expanding the logistics and export potential» [Vaganova О V , 2020].

References

- Current problems of taxation of agricultural businesses, 2019. Natural and humanitarian research No. 26 (4), 2019: 27-32.

- Antonova N., 2020. The Ministry of Agriculture has updated the rules for granting a unified subsidy from 2020 // Regulation gov.ru access mode: https://aftershock .news/?q=nodc/835259&full The draft government decree is published on the Regu- lation.gov.ru portal. (Accessed 5 May 2020).

- Bryzgalin A. V. Golovkin A. N., 2010. Complex operations and transactions taxation and accounting (part one). - Tax and Financial Law, 2010. https://base.garant.ru/55059771/(Accessed 5 May 2020).

- Declaration of the UCHN for 2019: instructions for filling out in 2019. Example - How to build your business [Electronic resource] Access mode: https://kmb-chr.ru/sposobv- zarabotka/deklaratsiva-eshn-za-2019-god-in- struktsiva-po-zapolnenivu-v-2019-primer.html (Accessed 5 May 2020).

- Federal Law of November 27, 2017 No. 335-FZ " On Amendments to Parts One and Two of the Tax Code of the Russian Federation and Certain Legislative Acts of the Russian Federation [Electronic resource]: Access mode: http://www.consultant. ru/document/cons_doc_LAW_283495/

- Unified agricultural tax in 2020: changes, rate. [Electronic resource]: Access mode:. https://www.rnk.ru/article/217060-eshn-v-2020- godu-izmeneniva/ (Accessed 5 May 2020).

- Vaganova О V, 2020. Transformation of Agriculture Through Digitalization, Innovative Solutions, and Information Technologies / O.V. Vaganova, N.E. Solovjeva, Y.L. Aulov, L.I. Pro- kopova // Advances in Economics, Business and Management Research, volume 137. Proceedings of the III International Scientific and Practical Conference "Digital Economy and Finances" (ISPC-DEF 202024 April 2020) ISSN 2352-5428, ISBN 978- 94-6252- 957-1. DOI https://doi.Org/10.2991/aebmr.k.200423.015.

- Voznyuk, EA Taxation as an instrument of state regulation of the agro-industrial complex / EA Voznyuk. - Text: direct, electronic // Young scientist. - 2016. - No. 30 (134). - S. 161-163. - URL: https://moluch.ru/archive/134/37223/ (Accessed 5 May 2020).

- Tax Code of the Russian Federation 2020 [Electronic resource] Access mode: https://vladrieltor.ru/nalkodeks

- The main directions of budgetary, tax and customs tariff policy for 2020 and for the planning period of 2021 and 2022. [Electronic resource]: Access mode: https://www.minfm.ru/ru/document/?Id4=128344-osnov-nyenapravleniyabyudzhetnoinalogovoiitamozhenno- tarifhoi_politiki_na_2020^god_i_na_20_planovyi_ periodov

- The Draft government decree was published on the portal Regulation.gov.ru. /(Accessed 5 May 2020).

- Subsidizing the agro-industrial complex in 2020 [Electronic resource]: Access mode: https://m- tv.ru/gos-podderzhka-apk-2020-g/ /(Accessed 5 May 2020).

- Zharova E.N. Current problems of taxation of agricultural commodity producers // Modem management technologies. ISSN 2226-9339. - No. 12 (24). Article number: 2405. Publication date: 2012-12-08. Access mode: https://sovman.ru/article/2405/ (Accessed 20 April 2020).

- Zhuravleva T.A. Unified agricultural tax and the reasons for its lack of demand by agricultural producers in Russia // Economy: yesterday, today, tomorrow. 2016 No. 3: 111-121.